Choosing the right health insurance plan is a critical decision that can have a significant impact on your healthcare experience and financial well-being. Among the most common types of health insurance plans are Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). Each of these plans offers unique advantages and potential drawbacks, and understanding the differences between them is essential for making an informed choice. In this article, we’ll compare HMO and PPO plans, exploring their key features, benefits, and considerations to help you determine which option is best suited to your needs.

What is an HMO?

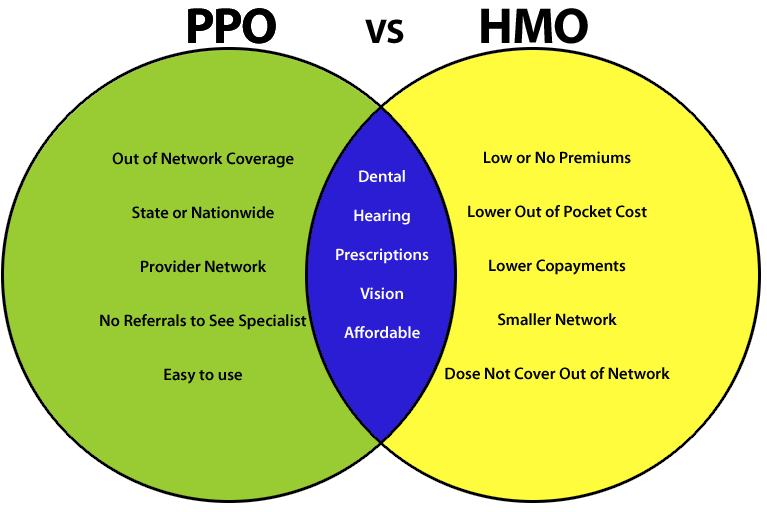

A Health Maintenance Organization (HMO) is a type of health insurance plan that provides coverage through a network of healthcare providers, including doctors, hospitals, and specialists. HMO plans are known for their cost-effectiveness and focus on preventive care. However, they come with certain restrictions that policyholders should be aware of.

Key features of HMO plans include:

- Primary Care Physician (PCP): HMO members are typically required to select a primary care physician who acts as the first point of contact for all healthcare needs. The PCP coordinates care and provides referrals to specialists within the network if necessary.

- Network-Based Coverage: HMO plans generally only cover services provided by healthcare providers within the plan’s network. If you seek care outside the network, you may have to pay the full cost out-of-pocket, except in emergencies.

- Lower Premiums and Out-of-Pocket Costs: One of the main advantages of HMO plans is their lower premiums and out-of-pocket costs, such as co-pays and deductibles. This makes HMOs an attractive option for individuals and families looking for affordable healthcare coverage.

- Emphasis on Preventive Care: HMO plans often emphasize preventive care, offering coverage for routine check-ups, vaccinations, and screenings. This focus on prevention helps to keep overall healthcare costs down.

What is a PPO?

A Preferred Provider Organization (PPO) is another popular type of health insurance plan that offers more flexibility in choosing healthcare providers. PPO plans allow members to receive care from both in-network and out-of-network providers, giving policyholders greater control over their healthcare choices.

Key features of PPO plans include:

- No Primary Care Physician Requirement: Unlike HMOs, PPOs do not require members to choose a primary care physician. You have the freedom to see any doctor or specialist without needing a referral.

- Flexible Provider Options: PPO members can seek care from both in-network and out-of-network providers. While staying within the network will save you money, you still have the option to receive care outside the network, albeit at a higher cost.

- Higher Premiums and Out-of-Pocket Costs: PPO plans generally have higher premiums compared to HMOs. Additionally, out-of-pocket costs, such as deductibles and co-insurance, may be higher, particularly when receiving care from out-of-network providers.

- Greater Autonomy in Healthcare Decisions: PPOs offer greater autonomy when it comes to making healthcare decisions. You can see specialists and receive treatments without needing approval or referrals, making it easier to access the care you need.

Comparing HMO and PPO Plans

When comparing HMO and PPO plans, it’s important to consider several factors, including cost, flexibility, network size, and your personal healthcare needs.

- Cost:

- HMO: HMO plans typically have lower monthly premiums and out-of-pocket costs. They are a good choice for individuals who want affordable coverage and are willing to work within a network of providers.

- PPO: PPO plans usually come with higher premiums, but they offer more flexibility in choosing healthcare providers. If you’re willing to pay more for the freedom to see out-of-network doctors or specialists, a PPO might be the better option.

- Network and Provider Access:

- HMO: With an HMO, you are limited to a network of providers. If your preferred doctors or specialists are within the network, this may not be an issue. However, if you frequently travel or have specific providers you want to continue seeing, the limited network could be a drawback.

- PPO: PPO plans offer a broader network of providers and the flexibility to see out-of-network doctors. This makes PPOs a good choice for those who value flexibility and have established relationships with healthcare providers who may not be in a single network.

- Referrals and Specialist Access:

- HMO: In an HMO plan, your primary care physician acts as a gatekeeper, and you will need a referral to see a specialist. This can add an extra step to receiving care, but it also ensures that your care is well-coordinated.

- PPO: PPO plans do not require referrals, allowing you to see specialists directly. This can be advantageous if you have ongoing health issues that require specialist care or if you prefer to manage your own healthcare without a PCP’s involvement.

- Preventive Care:

- HMO: HMOs often place a strong emphasis on preventive care, covering services such as vaccinations, screenings, and routine check-ups. This can lead to better overall health outcomes and lower healthcare costs over time.

- PPO: While PPOs also cover preventive care, they may not place as much emphasis on it as HMOs. However, the flexibility of PPOs allows you to choose where and from whom you receive your preventive services.

- Emergency Care:

- HMO: HMO plans cover emergency care even if it is received outside of the network, but you may need to notify your insurance company within a certain timeframe. Non-emergency care received outside the network is generally not covered.

- PPO: PPO plans provide coverage for emergency care received both in and out of network, offering greater peace of mind if you travel frequently or live in an area with limited in-network providers.

- Suitability for Different Individuals:

- HMO: HMOs are well-suited for individuals and families who want affordable healthcare, are comfortable with a network-based system, and do not anticipate needing frequent specialist care outside the network.

- PPO: PPOs are ideal for those who value flexibility, prefer not to deal with referrals, and are willing to pay higher premiums for the ability to see a wide range of providers, including out-of-network options.

Which Plan is Right for You?

Choosing between an HMO and PPO depends on your healthcare needs, budget, and personal preferences. Here are a few questions to consider when making your decision:

- Do you have a preferred primary care physician or specialist that you want to continue seeing? If so, check whether they are in-network for both HMO and PPO options.

- Are you looking for the most affordable plan? An HMO may be the better choice due to its lower premiums and out-of-pocket costs.

- Do you want the freedom to see specialists without a referral? A PPO offers more flexibility in accessing specialist care.

- How important is it to you to have nationwide or out-of-network provider access? If you travel frequently or live in a rural area with limited in-network providers, a PPO may be more suitable.

Both HMO and PPO plans have their own set of advantages and potential drawbacks. Understanding these differences is key to choosing the right health insurance plan for you and your family. Whether you prioritize cost savings, flexibility, or access to a broad network of providers, taking the time to compare HMO and PPO plans will help you make an informed decision that aligns with your healthcare needs and financial situation.

ghehoi.com offers expert advice and coverage options for all your insurance needs, ensuring peace of mind.

If you need advice on Comparing Health Insurance Plans: HMO vs. PPO please contact insurance.drozur.com for advice in the field of insurance worldwide:

Web: ghehoi.com

Add: 2500 WEST FWY, FORT WORTH, TX 76102-5852 USA

Email: insurance@ghehoi.com

Hotline: 088 526 489

Please read more articles, this is the content you need:

Why You Need Health Insurance and How to Get It

Health insurance plays a critical role in protecting both your health and your financial security. [...]

Sep

How to Switch Home Insurance Companies Without Losing Coverage

Switching home insurance companies is a common practice for homeowners looking to save money or [...]

Sep

How to Get Car Insurance Discounts: Tips and Tricks

Car insurance is a necessary expense for drivers, but that doesn’t mean you have to [...]

Sep

Understanding the Tax Benefits of Life Insurance

Life insurance is not just about providing financial protection to your loved ones in the [...]

Sep